LlamaRisk has not conducted a thorough risk evaluation of Falcon sUSDf, although we have done some internal due diligence and are in active communication with their team. sUSDf is a new asset that comes with several notable risks, some of which are described in this proposal. As with any onboarding, Resupply stakeholders are encouraged to conduct their own due diligence.

LlamaRisk has not received any compensation for this proposal and we present it to Resupply in our capacity of providing integrations support for Curve DAO.

Summary

Add the sUSDf-long LlamaLend market with vault address 0xFf771E92DD2400b4F2D3E0aC3AfAe3aE1885877E, allowing users to mint reUSD and leverage supply to the market.

Set the market with a max 95% LTV, 5% liquidation fee, and 3m reUSD max borrow.

sUSDf Overview

Falcon Finance enables whitelisted users to mint USDf from a variety of supported assets, including stablecoins and crypto assets. A detailed list of supported collateral for minting USDf can be found in their documentation here. Falcon uses delta-hedging strategies with capital deployed to centralized exchanges, and on-chain liquidity/staking pools, employing off-exchange custody services through its partner custodians.

The protocol offers sUSDf, a yield-bearing version of USDf, an ERC-4626 vault that accrues rewards from Falcon’s yield generation strategies. Users can stake their USDf into this vault, and in return, they receive sUSDf, which acts as a receipt token representing their share of the vault. Unlike Ethena’s sUSDe (an analogous product), sUSDf does not involve an unstaking cooldown period. Note that the vault contract does include functionality for setting a cooldown period, but the Falcon team have indicated no plan to introduce a cooldown. However, there is a one week delay on USDf redemptions, available to whitelisted users. Due to delays on arbitrage operations, USDf may not always maintain a strong 1:1 USD peg, and may exhibit similar market dynamics as sUSDe.

sUSDf is currently undergoing a gauge vote to receive CRV emissions and the vote is likely to pass. Additionally, Falcon Finance has an incentive program called “Falcon Miles.” The program uses points to reward users who interact and utilize Falcon Finance. More information on Falcon Miles can be found here.

Source: Dune

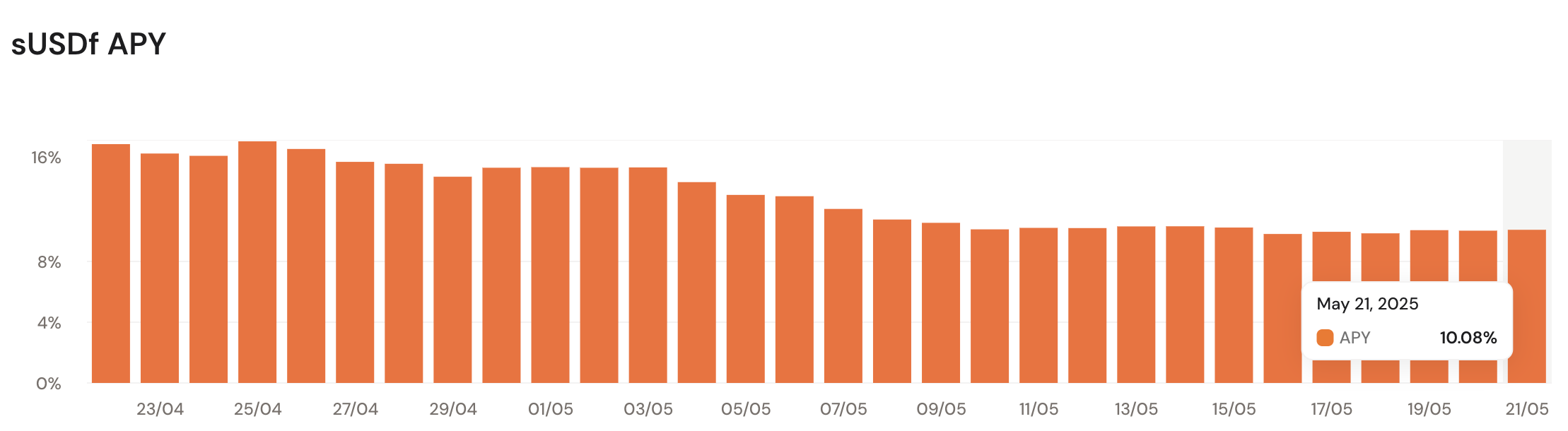

Since the beta launch on February 18, 2025, the sUSDf stablecoin has gained rapid adoption. Currently, there is 214 million sUSDf in circulation at a market cap of ~ $222 million.

sUSDf has yielded an average of 13.8% APY since launch. However, the yield has slowed considerably to ~ 10% APY currently.

Source: Falcon App

sUSDf Risks

There are several risks we have observed that may impact the solvency and/or stability of sUSDf. These include low asset maturity, high dependence on the team’s operational management, transparency concerns, and inclusion of broad and low quality collateral types in the reserves. These points constitute our initial observations and do not comprise a thorough risk evaluation.

- The Falcon team have unilateral authority over the operational management of the reserve assets. Insolvency may occur due to operational mismanagement or failure of underlying strategies which include exposure to CEX exchanges and DeFi strategies. As with analogous products, Falcon relies on off-exchange custodians to mitigate losses that may result from CEX insolvency.

- USDf can be minted using a wide range of altcoins, including DOLO- a very low cap token. Using DOLO as collateral, up to 50,000,000 USDf can be minted, which exceeds DOLO’s market capitalization of $14.2 million (as of 5/22/25).

- While Falcon provide a transparency dashboard that designates reserves denominated in stablecoins and crypto and managed by several custodians, it does not provide a complete breakdown of the reserve assets. This prevents USDf holders from having a complete understanding of the risk they are exposed to.

- The oracles used for collateral assets to mint USDf is unclear. Although Chainlink oracles are stated in the documents for USDf/USD and sUSDf/USD, it is not explicitly stated where price data for collateral assets come from. For users to deposit safely, oracle transparency is needed, especially when low marketcap altcoins are accepted as collateral. For instance, with the low liquidity for DOLO, oracle manipulation could lead to an attack on USDf.

- The addition of liquidity pool positions as stablecoin backing brings additional risks that come along with using another DeFi application. The DeFi applications that are being utilized by Falcon are not specified. This means that the overall risk profile of the yield generation cannot be known.

- Falcon’s docs reference arbitrage in the category of liquidity pools. It is unclear if the Liquidity Pool designation is limited to supplying to LPs or engaging in arbitrage or other sophisticated strategies.

- Falcon speaks of an insurance fund in their documents being verifiable on-chain. This insurance fund was not readily accessible to the public at the time of writing.

- There are two methods for minting USDf: the regular method and what they term ‘Innovative Mint’. The latter employs an unconventional mechanism involving transactions similar to both purchasing and selling call options, where collateral is forfeited if the price falls below a specified threshold. Concerns arise from the potential to incur losses and the system’s centralized nature, which obscures the transparency of its underlying processes.

- Competing products that do not have an unstaking cooldown have experienced issues with MEV value extraction upon rewards distribution. We have not verified if sUSDf is exposed to this risk or if they have implemented a system to prevent such extraction.

Market Configuration

LlamaRisk has deployed the sUSDf LlamaLend market. Given here is our rationale for the market configuration and recommendation on a suitable debt ceiling for the market.

Parameters

| Parameter | Value |

|---|---|

| A | 200 |

| AMM Swap Fee | 0.2% |

| Liquidation Discount | 1.4% |

| Loan Discount | 1.9% |

| Max LTV | 97% |

The market has been instantiated with the same market parameters as the sUSDe-v2 market in prod. USDf is a new product and very little history is available to refine specific attributes of this asset. However, given it is an analogous product with similar properties, the assumption of relatively similar market behavior to sUSDe is reasonable.

Running simulations with limited market history suggests that the market can support more aggressive parameterization, but market history does not account for potential depeg events due to the 7 day redemption timeline on USDf. For reference, simulations are given here:

Monetary Policy

| Parameter | Value |

|---|---|

| Min Rate | 0.1% |

| Max Rate | 25% |

The market uses Semilog Monetary Policy, the current standard for LlamaLend Markets. This policy uses a polynomial curve based on the market utilization and the min/max rates set by governance. The parameter config is consistent with other yieldbearing stablecoin markets and is intended to exceed the expected yield on the underlying, thereby protecting lenders against market illiquidity.

As sUSDf has historically yielded above market rates and is a new protocol, it may experience high yield volatility. If needed, rates can be modified for this market by the Curve DAO.

Oracle

The oracle used in LlamaLend markets is a critical dependency and typically employs one or more Curve pool price oracles to derive a market price for the underlying. The sUSDf oracle contract can be found here.

The oracle for sUSDf was deployed with a proxy, allowing the Curve DAO to set a new oracle implementation.

The underlying pools and contracts used in the oracle include:

- USDf/USDC: $12.5m TVL

- USDC/crvUSD: $26.2m TVL

- sUSDf vault

- crvUSD price aggregator

This TVL is enough to ensure a reliable price oracle and Falcon have stated an intention to maintain liquidity in these pools for the foreseeable future. However, active monitoring is necessary to ensure the pool continues to be a reliable price source. If the need arises to migrate the price feed, this market has been created with an oracle proxy that allows Curve DAO to change the implementation contract.

The use of aggregated price of crvUSD improves the resiliency of the market to instances of transient crvUSD depeg in the constituent pools. This reduces the probability that users can be liquidated as a result of crvUSD price deviations. Note that not all LlamaLend markets make use of the crvUSD price aggregator but it is now standard for all newly created markets.

Debt Ceiling

sUSDf is a yield bearing version of USDf, meaning it should apreciate in price. Multiple DEX aggregators suggest there is no active liquidity where swaps could be made. Hence, at the time of liquidations, the liquidator might not be able to sell the collateral to realize the profits, negating the liquidation all together.

This concern is eliminated by the fact that unstaking from sUSDf to USDf is immediate, as quoted by the protocol docs. Since unstaking is facilitated spontaneously, USDf liquidity is analyzed to gauge the market depth and quote an initial debt ceiling. Note that the introduction of an unstaking cooldown would break our assumption of a safe debt ceiling.

Given the market parameterization:

"market": sUSDf-long

"liquidation_discount": 14000000000000000, # i.e. 1.4%

"loan_discount": 19000000000000000, # i.e. 1.9%

"amm_a": 200,

The most conservative quote here would be answering the following question, how much USDf needs to be sold into crvUSD to realize a price impact of 1.4%?

In current conditions, this is around 3,480,000 USDf i.e. ~3,364,000 @ 1.0346 exchange rate. Considering an average overcollateralization of 111.11%, the debt ceiling comes out as 3,480,000/1.111 = 3,132,000 crvUSD.

With the above debt ceiling, the market will be able to absorb 100% of debt positions all at once, even at a 100% debt ceiling utilization. 100% market utilization is unlikely to occur, and it is a conservative assumption. If we assume a target utilization of 70%, the debt ceiling can be increased to ~4,500,000 crvUSD.

With the soft-liquidation mechanism in place, collateral will gradually be swapped into crvUSD, reducing the overall collateral getting released in the market due to liquidation. This adds conservativeness to the quoted ceiling.

Due to the asset maturity and risk considerations, we propose a very conservative preference in setting the debt ceiling for this asset, arriving at a recommendation for 3m reUSD cap at this time.